In your opinion, What are some essential knowledge areas that every business owner should have a grasp of? Accounting principles and standards are the foundation of financial reporting for businesses. They provide a framework for recording, classifying, and summarising financial transactions and ensure that financial statements are accurate and reliable.

Every business owner should have a basic understanding of these principles and standards in order to make informed decisions about their finances. And more, in a sense, they should have a basic understanding of these accounting principles and standards in order to make informed decisions about their finances. This includes understanding how to read and interpret financial statements and how to use financial data to make business decisions. Business owners should also work with a qualified accountant or financial advisor to ensure that their financial reports are accurate and compliant with all applicable laws and regulations.

A brief overview of Accounting Standards

The International Financial Reporting Standards (IFRS) and the Generally Accepted Accounting Principles (GAAP) are the most widely recognised accounting standards. IFRS was developed by the International Accounting Standards Board (IASB) and is used in over 130 countries around the world. On the other hand, GAAP was established by the Financial Accounting Standards Board (FASB) and is primarily used in the United States.

One of the key principles of accounting standards is the accrual basis of accounting. This principle states that businesses should record revenue and expenses when they are earned or incurred rather than when they are received or paid. This ensures that financial statements accurately reflect the financial performance of the business over a period of time.

Another important principle is the consistency principle, which states that businesses should use the same accounting methods from year to year unless there is a good reason to change them. This ensures that financial statements are comparable from one year to the next.

In addition to these principles, accounting standards also provide guidelines on recording and reporting specific types of transactions, such as inventory, property, plant, equipment, and leases. Business owners should work with a qualified accountant or financial advisor to ensure that their financial reports are in compliance with these standards. And in addition to that important aspect of accounting standards is the required disclosure in financial statements. The standard requires companies to provide information about their financial performance, financial position, cash flows, and other matters that may affect their ability to continue as a going concern.

Accounting standards are the set of guidelines that businesses must follow when preparing and presenting their financial statements. They ensure that financial statements are accurate, reliable, and comparable across different companies and industries. Every business owner should have a basic understanding of these standards in order to make informed decisions about their finances and comply with legal requirements. It is also important to work with a qualified accountant or financial advisor to ensure that financial reports are in compliance with these standards.

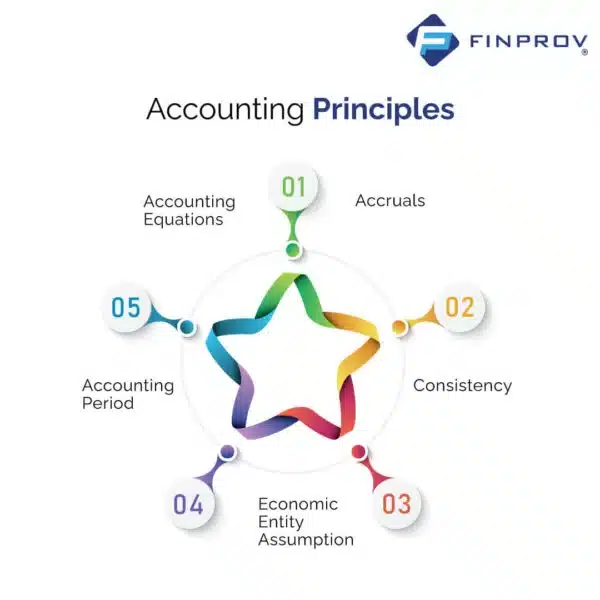

Take a look at Accounting Principles

Understanding major accounting principles help a business for crafting and implementing the best financial statements. For the prediction of accounting sales and cost and financial statement preparations, knowing the accounting principles plays better preparation.

Accruals

The Accrual basis method of accounting matches the income and expenses to the specific periods in which they are incurred, regardless of when the payment is received or made. As an example, an invoice is considered accounts receivable as soon as it is sent out. On the other hand, the Cash basis method records only the income and expenses when they are received or paid. Using this method, income will be recorded only when an invoice is paid, and accounts receivable are not considered.

Although small businesses often begin with cash basis accounting, accrual basis financial statements provide a more comprehensive understanding of the business’s financial position. Moreover, companies that are publicly traded are required by Generally Accepted Accounting Principles (GAAP) to use the accrual accounting method.

Consistency

The concepts propose nothing but the need to stick to the chosen accounting methods for all financial records, including the future. The consistency concept points out that the actions help to accurately assess organisational financial performance for different accounting periods.

Economic Entity Assumption

An important principle in accounting that emphasises the separation of business and personal finances. It states that a business’s financial statements should only include transactions that pertain to the business, not personal transactions of the owners or employees. This means that personal expenses should not be mixed with business expenses, for instance, by using a business credit card for personal purchases. Adhering to this principle is crucial for accurate online bookkeeping and for maintaining the legal status of corporations and limited liability companies, which require a clear separation of business and personal finances to preserve limited liability protection.

Accounting Period

This concept refers to the practice of including only financial records pertaining to a specific period in the financial statements. This principle is applied to the three main financial reports; the Profit and Loss Statement, the Balance Sheet, and the Statement of Cash Flows. These reports cover different time periods, such as a quarter or a calendar year, and are used to evaluate the performance of the business during that time. For example, a Profit and Loss statement made for the first quarter of the year would only include transactions that occurred within that quarter and not before or after it. This allows the company to accurately compare its performance over different time periods and make informed decisions.

Accounting Equations

The Accounting Equation is a fundamental principle that helps to understand how financial transactions are recorded in accounting software. It states that:

Assets = Liabilities + Owner’s Equity

This equation shows that the total assets of a business must be equal to the total liabilities and owner’s equity. In other words, all the resources owned by a business must be financed either by borrowing money or by using the money invested by the owner(s).

In this equation, Assets are recorded on the left side and debited in the general ledger. For example, when a business receives cash, the accounting software debits the cash account. On the other hand, Liabilities and Owner’s equity are recorded on the right side, and they are credited in the general ledger. For example, when a company issues shares of common stock, the software credits the owner’s equity account with the corresponding amount.

Like the wise, Materiality concepts, which are regarding the records of the financial transactions, matching concepts related to the relationship between the income and purchase of a firm, etc., more accounting principles are there which a firm has to consider during its functioning. For smooth financial performance and success, a firm must be aware of accounting standards and principles. Every business owner should have a basic understanding of these standards in order to make informed decisions about their finances and comply with legal requirements.

Familiarising with business laws, tax systems, and accounting softwares makes an organisation strong in financial performance. The successful functionality of the firm will be possible through dealing with these aspects, which helps to better understand accounting principles and standards both in practical and theoretical aspects. Finprov, the best accounting institution, helps you to become familiar with accounting principles through the most valuable courses. For our learners, we offer opportunities to acquaint them with Basic Business laws, GST, UAE VAT, Practical Accounting, Tally Prime, Zoho books, and MS Excel, like short-term courses. Finprov allows the aspirants to become an expert in accounting with practical experience. The advanced lab facilities with expert faculty support are an added plus for aspirants at Finprov.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}