Tax filing is a significant task to undertake, although it plays a crucial role for both individuals and businesses. One of the central steps is filing Income Tax Returns (ITR) each year. However, in the presence of different ITR forms available in the market, determining the best that fits the type of income and the nature of your operations might be a challenge. Relax, you are not the only one.

Here on this blog, we make it simple. Through learning when it is necessary to file ITR, different types of ITR forms and how to pick the correct ITR form, we have got your back to make tax season a little lighter.

What is ITR?

Income Tax Return or ITR refers to the income and tax reporting of taxpayers to the Income Tax Department, which mentions the income and tax paid by a taxpayer in a particular financial year. It is a legal obligation as defined in the Income Tax Act of 1961, and in case of non-filing or erroneous filing, the legal consequences include a penalty and the possibility of lawsuits.

Among other things, an ITR also contains details of deductions and taxes paid and refunds due, in addition to the amount of income and tax liability. These forms are of various types depending on the types of taxpayers (according to the source of income and type of income earned).

The filing of the ITR is annual and is required to be duly filed by individuals, Hindu Undivided Families (HUFs), companies, firms and other persons whose liability falls under the purview of the Income Tax Act. Different taxpayers have different deadlines for filing ITR depending on the category and the mode of filing. E-filing of ITR is another phenomenon that has gained popularity in recent years because it is quicker, convenient, and assists in reducing the possibility of error when sending or filling in the documents.

Taxpayers should also consider appropriate and consistent ITR filing since failure to do so would lead to penalties, fines, and even court proceedings. Besides, by filing ITR, taxpayers are able to file their income, which is valid in the acquisition of loans or other types of visas, and other financial necessities.

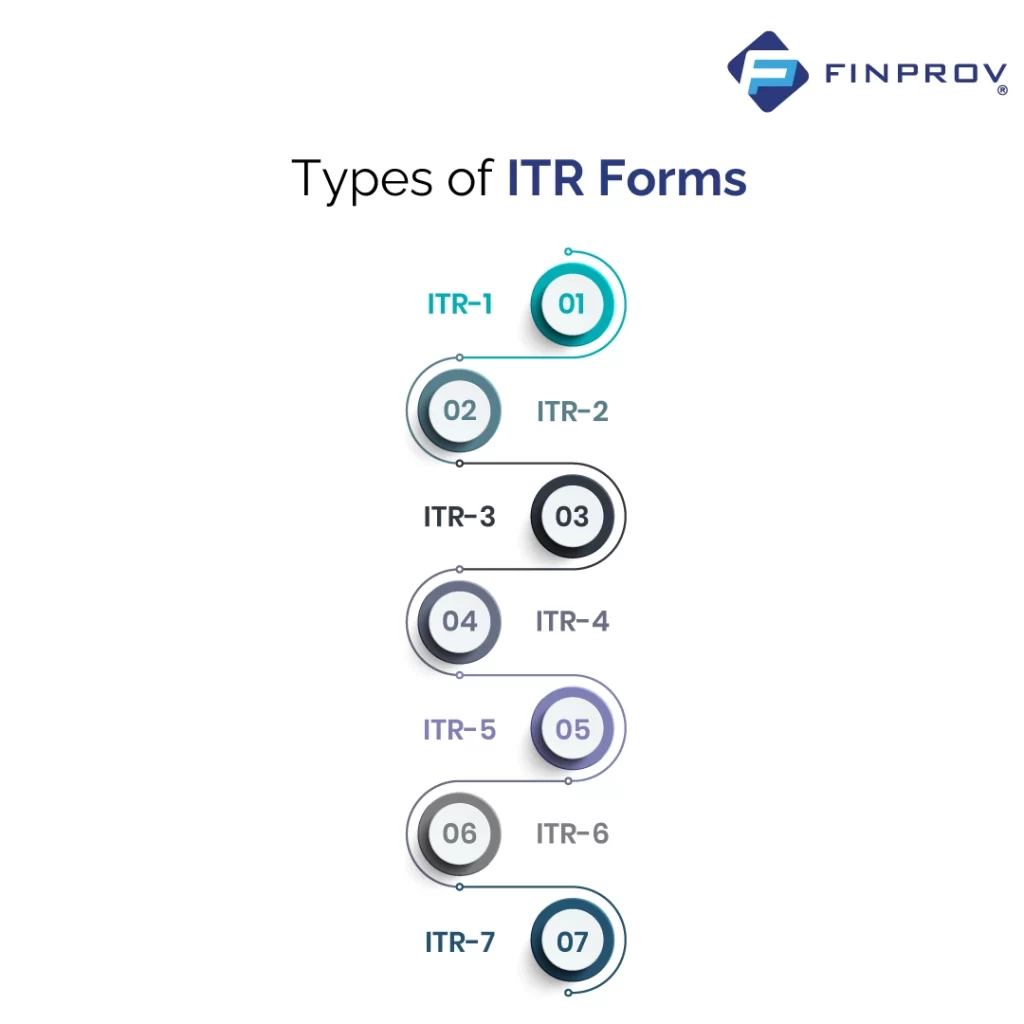

Types of ITR Forms

The ITR form varies depending on the nature of income, business or profession and the total amount of compensation that one earns in one financial year. The Central Board of Direct Taxes or CBDT has stipulated seven varieties of these forms depending on the nature of the taxpayer.

ITR-1: For people with Income from One House Property, Salaries, and Other Sources, and having a Total Income up to Rs 50 lakhs.

The most direct and widely used is the Sahaj form, ITR-1. It applies to the people whose income is in terms of salaries, one house property, and other sources totalling up to INR 50 lakhs. Nevertheless, it may not be filed by those who are the directors of a company or have invested in the unlisted equity shares or have gained capital gains over the year.

ITR-2: The ITR-2 would be used by individuals and Hindu Undivided Families (HUFs) for not conducting business or profession under any proprietorship. It can also apply in the case where one possesses multiple house properties, a person has earned capital gains in the year, or one has foreign assets or income.

ITR-3: This refers to a person or a Hindu Undivided Family member who is a partner to firms without practising any business or profession as a sole proprietor. The form is also suitable where individuals and HUFs derive their income from innovation through proprietorship in the business or professions.

ITR-4: Individuals and HUFs with Presumptive Income -ITR 4 or Sugam is aimed at individuals and HUFs whose income is in the form of presumptive business or profession. In case your income is computed on a presumptive basis as under any one of the following sections of the Income Tax Act: 44AD, 44ADA, or 44AE, then this form is applicable in your case.

ITR-5: This form is suitable for partnerships, LLPs, and the Association of Persons (AoPs). It can be filed only online.

ITR-6: This type is appropriate for such companies that are not exempted according to Section 11 of the Income Tax Act and are filed only online.

ITR-7: This return form is applicable to those entities that must provide returns in any of the specified sections in the Income Tax Act: Section 139 (4A), Section 139 (4B), Section 139 (4C) or Section 139 (4D). The form is only filed online.

Which ITR should you file?

If you are an Indian taxpayer, it is important to file your Income Tax Returns (ITR) accurately and on time. ITR filing is a major responsibility that every individual or entity earning taxable income must fulfil. However, with several types of ITR forms available, it can be confusing to determine which ITR form to file.

Let’s discuss which ITR form you should file based on your financial situation:

Salaried Individuals: If you have a salary income, income from a single property, or income from other sources, you should file ITR-1. However, if you have income from multiple sources, including salary, house property, capital gains, and foreign assets, you should file ITR-2.

- If you have a salary that comes from a single property income or other income, you should submit the ITR-1 form.

- If you earn income other than salary, such as house property, capital gains and income abroad, you have to use ITR-2.

- In case you earn any income in the form of salaries, pensions or interest and whose sole income is such, then you can also file your ITR through Form ITR-1 (SAHAJ).

- Assuming that your only form of income is capital gain, house property or foreign assets without any other means of income, then you are allowed to submit your ITR in Form ITR-2.

- In case you are receiving income in the form of a sole proprietorship business or profession, then you may file your Income Tax Return (ITR) under Form ITR-3.

- In case you do not want to go into the details of reporting your income, you just pay a predetermined amount of taxes based on your business or profession and file your ITR using Form ITR 4 (SUGAM).

- Filing ITR under Form ITR 5 can be done only by LLPs, AOPs, BOIs and partnership firms.

- You can use Form ITR-6 to file your ITR, provided you are not companies that claim exemption under section 11.

- Suppose you have the obligation of the furnishing return u/s 139(4A), 139(4B), 139(4C), and 139(4D) and you can file your ITR, by using Form ITR-7.

Let’s take a quick overview with the given table:

| ITR Form | Eligible Taxpayers | Non-Eligible Taxpayers |

| ITR-1 | Resident and Ordinarily Resident (ROR) individuals with an income up to 50 lakh, including the income of their spouse or minor child. | Those individuals who gross more than Rs. 50 lakh, earn income out of a number of house properties or earn income in terms of business or profession. |

| ITR-2 | Individuals and Hindu Undivided Families ( HUFs ) who are unable to file ITR-1 and have income by way of salary, house property, capital gains, and foreign assets. | Individuals and HUFs having income from business or profession, or presumptive income under section 44 AD, 44ADA or 44AE. |

| ITR-3 | Individuals and HUFs income from business or profession, including those in a partnership firm. | Individuals and HUFs without income from business or profession. |

| ITR-4 | Assessee Individual, HUF, and firm (other than LLP), who have a presumptive income under business or profession. | ITR-4S cannot be filed by companies, LLPs, trusts, or other institutions. |

| ITR-5 | Other persons or entities other than individuals, HUFs and companies that file ITR-7 (e.g. LLPs). | HUFs, individuals and companies that can submit ITR-1, ITR-2, ITR-3, and ITR-4. |

| ITR-6 | Firms that do not seek exemption under section 11 of the Income Tax law. | Companies that apply an exemption under section 11 of the Income Tax Act. |

| ITR-7 | Individuals such as companies, charitable and religious trusts, political parties, universities, colleges and other specified persons. | Persons, HUFs, and firms in a position to submit ITR-1, ITR-2, ITR-3 and ITR-4. |

It is worth putting on record that yearly eligibility requirements of different types of ITR forms may change, and the taxpayers must ensure that they confirm the latest updates before making their returns. It is applicable, as a person in accounting and the general populace, to have knowledge of ITR. But in order to master income tax, GST and the rules and regulations related to the government, it is equally important to read the latest changes and developments. Individuals can stay informed by reading books and articles, receiving news with the help of newsletter subscriptions, attending events, such as seminars, webinars, and following the official websites of the tax authorities.

Furthermore, access to practical-oriented training is also a very significant factor in attaining skills and being competitive in the job market. One can earn enrollment in a respected training program, which can give them an opportunity to work on real-life situations and problems.

Finprov is an excellent option for individuals seeking to update and upgrade their skills in GST filing, income tax, Gulf VAT, and accounting software. Our training modules are designed based on real case studies, providing participants with a practical understanding of the concepts.

Additionally, accounting professionals can also benefit from gaining expertise in popular accounting software such as SAP FICO, Tally Prime, MS Excel, and more. These software programs can help individuals streamline their accounting processes and increase their efficiency at work.

FAQs:

Q1. What is ITR-1 Sahaj?

ITR-1 Sahaj, the simplest ITR Form available to the salaried persons whose income does not exceed Rs. 50 lakhs combined with other sources of income.

Q2. For whom is ITR 2 applicable?

ITR-2 should be used when the income of the person or HUF does not arise out of business or profession, in case of the individual, and where the total income of the individual includes income of more than one house property or income of more than one capital gain.

Q3. What to do to receive a tax refund and a TDS refund in accordance with the Income Tax Act 87A?

In case your total income after deductions and exemptions is less than 5lakhs, you can access the refund of the amount you will pay as per tax. Maximum Refund Rs. 12,500. Also, if you have paid TDS(Tax Deducted at Source) on your income, then you can also be subject to a refund.

Q4. Can I file an Income Tax Return (ITR) in case I incur losses through a job, home or a sale of stocks?

Yes, it does qualify to file an ITR, although one may have an earning activity of job loss, sales of stocks or home loan interest. By filing an ITR, there is the ability to claim losses in cases that you carry forward to future years in order to set off the future income. Nonetheless, you should produce your ITR within the stipulated time as given by the Income Tax Department.

Q5. What if I choose the wrong ITR form?

If you file the wrong ITR form, the Income Tax Department may mark your return as defective. You’ll get a notice to fix it within a certain time. If you don’t correct it, your return may be treated as not filed at all, and you could face penalties or other issues. That’s why it’s important to choose the right form based on your income and job type.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}